On the About YOU! page we introduced creating your own financial plan as Step 1 of how Life Financial Solutions assists you in wrapping your arms around your money.

This is based on the idea that you can't fully exercise your financial power without knowing what you're working with. You ever heard the business adage that you can't manage what you can't measure?

All through life and our working years, we're surrounded by talk of saving and retiring and financial market performance. But what's all this really add up to? And why do a lot of opinions and rules of thumb often bring more confusion than clarity?

This can all sound fairly stressful and depressing.

There's validity to the sentiments, positive and negative. Perhaps the biggest stressor of all is when the conflicting advice makes us think we thought we understood and believed the "right" thing to do but then it's ridiculed as wrong-headed or not enough. One person's trusted advice is not another's. And so on...

Then we learn it's not enough to just think about it -- we actually need to do something. And we wait because that's easier than trying to sort it all out or pay somebody to help us. And time goes by. And time lost is opportunity lost. But rushing can also be costly. So, what to do?

This page won't answer all those questions or solve all those problems. This is meant to stir your thinking with some ideas. As far as "resources," perhaps the greatest is knowledge. This page intends to get you to (1) think, (2) question your assumptions, and (3) challenge some myths.

The real resource for you is a well-crafted financial plan that becomes the conversation piece for greater learning and understanding. What if you could know enough, well enough, that you could be your own advisor? At the very least, how about being able to tell when something somebody says you should do is just not the right thing for you? This web site is not like a book you read to get all the answers and understand everything. That's what our conversations are for. What we talk about will be more targeted exactly to you and your circumstances.

So, go, now, and spend just a few minutes making that financial plan. You'll simply need to enter some important information, as completely and accurately as you can. Then we'll have charts and numbers to discuss from the resulting analysis. The only cost for you doing this is your time. You won't pay a dime!

1. The Power of Life Insurance

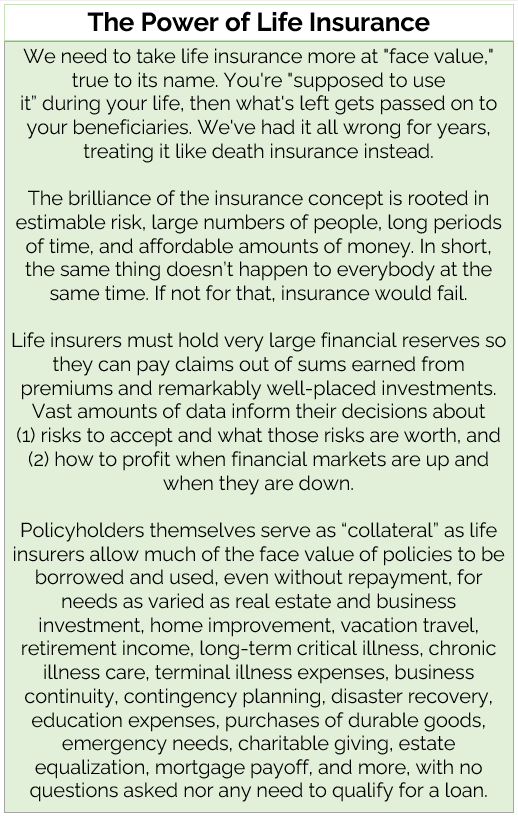

We need to take life insurance more at "face value," true to its name. You're "supposed to" use it during your life, then what's left gets passed on. We've had it all wrong for years, treating it like death insurance instead. (more...)

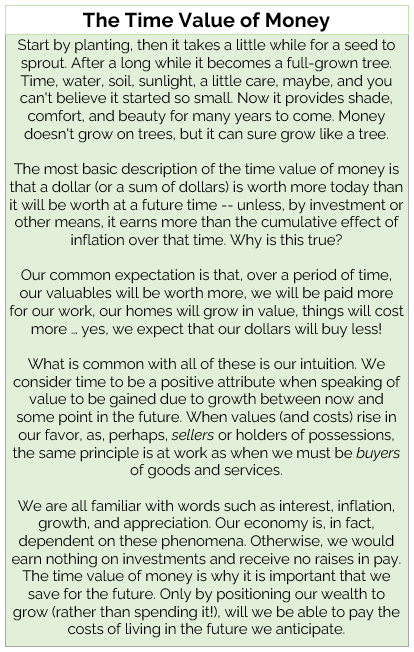

Start by planting, then it takes a little while for a seed to sprout. After a long while it becomes a full-grown tree. Time, water, soil, sunlight, a little care, maybe, and you can't believe it started so small. Now it provides shade, comfort, and beauty for many years to come. Money doesn't grow on trees, but it can sure grow like a tree. (more...)

Are you making money or losing money? How do you know? Got any money saved? Is that money earning at least as much as the current or average rate of inflation? What is the "real value" of the goods and services you buy, compared to what you actually pay? Can you buy as much as you could this time last year, at the same price? (more...)

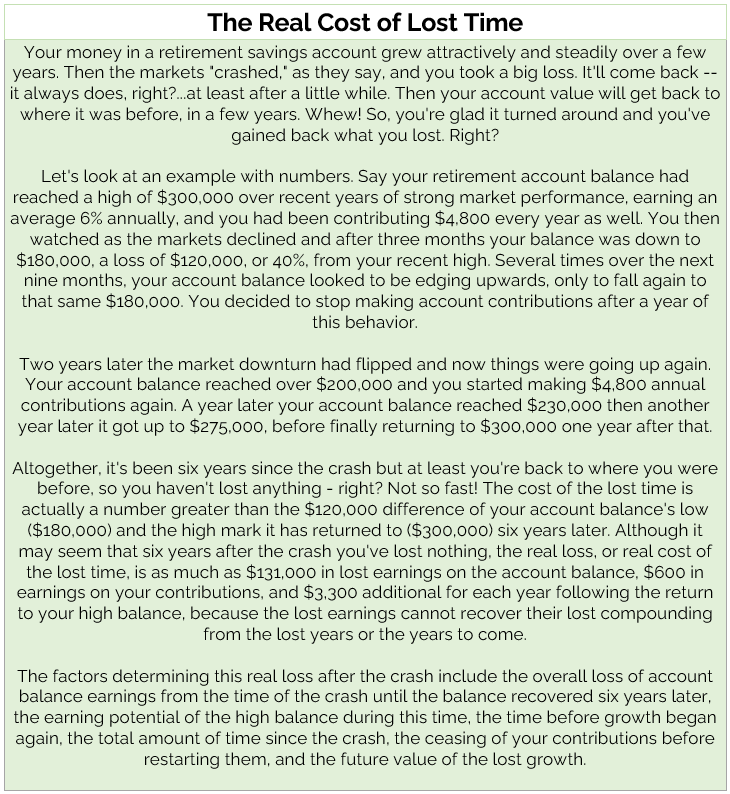

Your money in a retirement savings account and in your separate investment account grew attractively and steadily over a few years. Then the markets "crashed," as they say, and you took a big loss. It'll come back -- it always does, right? At least after a little while. Then your account value will get back to where it was before, in a few years. Whew! So you're glad it turned around and you've gained back what you lost. Right? (more...)

5. How Much Should I Really Have Saved?

Altogether, I've got more than $400,000 in my retirement accounts--that's a really nice sum. I should be okay. It's a big number. Plus, I'll get Social Security. And a pension. Why do I keep hearing that I may need three times this much when I stop working? (more...)

In the early days, you were just making it--training or school cost money, then you had loans to pay. You started living on your own and that got expensive. Then came the family, a bigger house, regular costs of living and trying to finally enjoy life as an adult. Now you save a little. You've heard you should save more...but how? Where's it supposed to come from? Plus, you'll have more time later. And more money. (more...) [See chart]

You've got your savings in the retirement account at work, your own personal investment account on the side, and some mutual funds with your friend, who is a broker. You're really good about saving. People you know have mentioned other things you might consider doing but you've already got diversification because you know "it's not good to have all your eggs in the same basket." (more...)

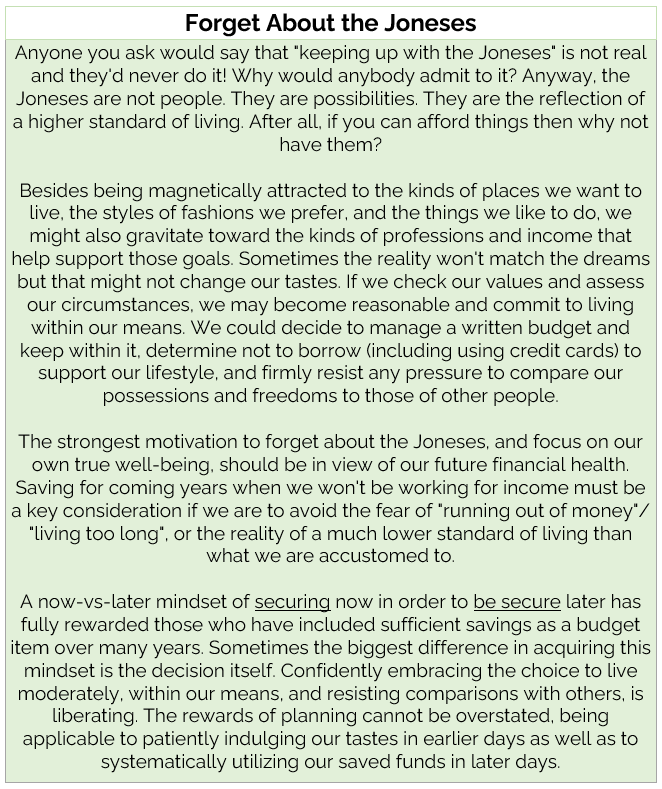

Anyone you ask would say that "keeping up with the Joneses" is not real and they'd never do it! Why would anybody admit to it? Anyway, the Joneses are not people. They are possibilities. They are the reflection of a higher standard of living. After all, if you can afford things then why not have them? (more...)

9. Simple Vs Compound Interest

If you earned 4 percent simple interest on $1,000, every month, in a year's time you would have $1,480. If you earned 4 percent compound interest on $1,000 every month, in a year's time you would have $1,601, which is $121 more. Why this difference? (more...)

10. Cash Flow

Try thinking of a large pipe with liquid money flowing from left to right. Inside the pipe, along its bottom surface, are many different-sized valves that let liquid out as it flows through. At the very top of the pipe are a few larger holes letting new liquid in. Sometimes the liquid reaches near the very top inside the pipe and sometimes the level is closer to the bottom. So, even though there is always some liquid in the pipe, the level goes up and down again as liquid comes in and goes out. At any snapshot of time, the "net flow" is the sum of what is already in the pipe plus what is coming into the pipe minus what is leaving the pipe. Imagine money flowing like this. (more...) [Get budget worksheet]

Learn why gold and silver...

Connect to alternative, noncorrelated investments

Get a referral for registered securities

Discuss digital currencies

Understand loans from life insurance

These are tax-deferred investment savings plans that allow you to postpone paying taxes on the money invested until it is withdrawn, generally after retirement. The names of the plans come from sections of the U.S. tax code pertaining to different types of employers. Employers often match a portion of your contributions.

Descriptive definitions adapted from Investopedia (https://www.investopedia.com/)

An annuity is an insurance contract issued by financial institutions with the intention of paying out invested funds in a fixed income stream in the future (the “distribution phase”). Funds are invested in a lump sum or in periodic premiums as funds grow during the “accumulation phase.” Annuities help individuals address the risk of outliving their savings.

A bond is a type of loan. When an issuer (e.g., company, government) needs funds for any number of reasons, they may issue a bond to finance that loan. Much like a home mortgage, they ask for a certain amount of money for a fixed period of time. When that time is up, the company repays the bond in full. During that time the company pays the investor a set amount of interest.

Cash is legal tender that can be used to exchange goods, debt or services. Although it typically refers to money in hand, the term cash is also used to indicate money in banking accounts, checks, or any other form of currency that is easily accessible and can be quickly turned into physical cash.

A collectible is an item worth far more than it was originally sold for because of its rarity and popularity, as well as its condition. Examples are coins, comic books, stamps, antiques, and art. Collectibles have appreciation potential and may be items that can be passed down to future generations. They may also provide some diversification benefits to an investment portfolio.

A cryptocurrency is a form of digital asset based on a network that is distributed across a large number of computers. This decentralized structure allows cryptocurrencies to exist outside the control of governments and central authorities.

An exchange-traded fund (ETF) is a type of pooled investment security that operates much like a mutual fund but can be traded like a stock. Typically, ETFs will track a particular index, sector, commodity, or other assets. They can contain investments including stocks, commodities, or bonds.

Precious metals are rare commodities which have long been valued by investors, which were historically used as a basis for money. Their economic value comes from their scarcity, use in industrial processes, hedge against currency inflation, and their role over time as a store of value. They are traded mainly as a portfolio diversifier.

A hedge fund is an investment partnership that invests aggressively and in a wider variety of financial products than most mutual funds. A professional fund manager is often known as the general partner and the investors as the limited partners. Together, they pool their money into the fund.

Individual retirement accounts (IRAs) are long-term retirement savings accounts with tax advantages for individuals with earned income. Types of IRAs include traditional IRAs, Roth IRAs, Simplified Employee Pension (SEP) IRAs, and Savings Incentive Match Plan for Employees (SIMPLE) IRAs.

Infinite banking is governed by section 7702 of the U.S. Code, and gives a life insurance policyholder the option to "overfund" their policy as a savings component. This allows them to make cash withdrawals during their life for investments, purchases, and income as the policy's cash value continues to grow. It is also known as "being your own bank," and called a 702(j) Plan.

Life insurance is a contract between an insurer and a policy owner. A life insurance policy guarantees the insurer pays a sum of money to named beneficiaries when the insured dies in exchange for the premiums paid by the policyholder during their lifetime. Today's life insurance policies can also provide benefits during the insured's lifetime.

A master limited partnership is a hybrid legal entity, a business venture in the form of a publicly traded limited partnership. It combines the tax advantages of a private partnership with the liquidity of a stock, paying out tax-sheltered distributions to the general partners and limited partners who are its investors.

A mutual fund is a financial vehicle that pools assets from shareholders to invest in securities like stocks, bonds, money market instruments, and other assets. A mutual fund's professional money managers allocate the fund's assets, attempting to produce capital gains for the fund's investors.

Tradable commodities are usually categorized by four basic groups: energy, metals, livestock, and agriculture. Among economists, there is little differentiation between a tradable commodity from one producer versus that from another source. This is different from products such as electronics, for example, where quality may be very different from one brand to another.

A pension plan is an employee benefit committing an employer to make regular contributions to a pool of money set aside to fund payments to eligible employees after they retire. Traditional pension plans are increasingly rare in the U.S. private sector, being largely replaced by retirement benefits less costly to employers, such as the 401(k) retirement savings plan.

Private debt is offered as an "alternative" investment in companies seeking funds for startup, expansion, or capital acquisition. Such companies, with strong credit, offer lucrative opportunities and pay investors very attractive stated interest rates along with timely repayment of invested funds. Such alternative opportunities are privately offered to qualified investors.

Private equity is offered as an "alternative" investment in companies seeking funds for startup, expansion, or capital acquisition. Investors become owners of shares of equity in the company and expect an attractive return on investment over time. They participate in company decisions and share profits. These opportunities are often offered privately to qualified investors.

A Roth IRA is a tax-advantaged account that allows you to pay taxes on contributions now and get tax-free withdrawals later. With a Roth IRA, your retirement distributions won’t be affected by unknown, evolving tax rates in the future. Roth IRAs function more like regular investment accounts, only with tax benefits. They have fewer restrictions, but fewer breaks as well.

A savings account is an interest-bearing deposit account held at a bank or other financial institution. These accounts typically pay a modest interest rate but provide a good option for emergency or short-term cash. The interest earned on a savings account is considered taxable income. The amount that can be withdrawn from a savings account is generally unlimited.

Stock shares are securities representing equity ownership in a corporation. Shareholders exchange capital in return for the ownership of a fraction of the value of the issuing corporation. Stock ownership anticipates growth in the company's stock price with increased performance and profits. Stocks are one of many different securities offered on public securities exchanges.

Structured products are pre-packaged investments that normally include assets linked to interest plus one or more derivatives. These products may take traditional securities such as investment-grade bonds and replace their usual payment features with non-traditional payoffs. The risks associated with structured products can be fairly complex and they tend to lack liquidity.

A unit investment trust, or UIT, is a financial company that buys or holds and offers to investors a fixed portfolio of securities, such as stocks and bonds, as redeemable units for a specific period of time. It is designed to provide capital appreciation and/or dividend income. Unit investment trusts, along with mutual funds and closed-end funds, are defined as investment companies.

Money market savings accounts are offered by banks and credit unions and provide the benefits and features of both savings and checking accounts. They generally pay higher interest rates than regular savings accounts and may come with debit cards and limited check-writing privileges while they may also impose more restrictions than regular savings accounts.

Real estate investment can include the purchase of physical structures as well as completely undeveloped land and property. Advantages include portfolio diversification, long-term passive income, tax benefits, and value appreciation. Many and various ways of investing in real estate can present different risks and opportunities, as distinct factors affect prices, values, and returns.

(Tap pie-slice icon

to return here.)

Tap here to listen to the content in this section

A little financial knowledge is a great financial resource.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

![[See chart]](https://files.secure.website/wscfus/10693093/30877265/the-timing-of-two-savers.png){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}